Summary

- Bulgaria has a flat 10% corporate and personal income tax rate, making it highly competitive within the EU. The country also offers a 5% dividend withholding tax, a 20% standard VAT rate, and specific social security obligations. These features create a predictable, low-tax environment that supports sound financial planning and business growth.

Tax in Bulgaria is defined by a flat 10% rate applied to both corporate and personal income, making it the lowest corporate tax rate in the European Union. For businesses and entrepreneurs evaluating EU jurisdictions, this structure offers a degree of predictability that progressive-bracket systems simply cannot match. Bulgaria’s regime also includes a 5% dividend withholding tax, a standard 20% VAT rate, and clearly defined social security obligations. Understanding each component is the foundation for sound financial planning and full regulatory compliance in 2026.

What are the main components of tax in Bulgaria for businesses?

Bulgaria’s tax framework is built on four pillars: corporate income tax, personal income tax, social security contributions, and VAT. Each operates under fixed rules that apply uniformly to resident companies and, in certain cases, to non-resident entities earning Bulgarian-source income.

Corporate income tax

The corporate tax rate is a flat 10%, with no minimum tax and no alternative minimum calculation. This rate applies to the taxable profit of resident companies on their worldwide income. Non-resident companies are taxed only on income sourced within Bulgaria. The distinction between resident and non-resident status is critical: a company incorporated in Bulgaria or managed from Bulgaria is treated as a tax resident and subject to the full scope of Bulgarian corporate taxation.

Personal income tax

Personal income tax in Bulgaria is also a flat 10%, with no progressive brackets and no tax-free threshold. Resident individuals pay this rate on worldwide income, while non-residents pay only on Bulgarian-source income. For business owners who draw a salary from their Bulgarian company, this flat rate applies directly to that compensation, eliminating the complexity of marginal rate calculations common in other EU states.

Social security contributions

Social security obligations are shared between employer and employee. Employee contributions total 13.78% of gross salary, while employer contributions range from 18.92% to 19.62%, depending on the nature of the business activity. These rates cover pension, health insurance, and other statutory funds. For payroll planning, the combined employer and employee burden represents a significant addition to the nominal salary cost and must be factored into total compensation budgets.

VAT structure and registration

The standard VAT rate is 20%, consistent with the EU average. A reduced rate of 9% applies to hotel accommodations, baby food, books, and certain housing transactions. Businesses must register for VAT once annual turnover exceeds EUR 51,130. This threshold is relatively low by Western European standards, meaning most active trading companies will reach it quickly and must plan for VAT compliance from an early stage.

Dividend withholding tax

The dividend tax rate is fixed at 5% in 2026, despite earlier budget proposals that suggested a potential increase. The combined effective tax burden on distributed profits, calculated as 10% corporate tax plus 5% dividend tax, amounts to 14.5%. This total remains competitive against most EU member states, where combined corporate and dividend tax burdens frequently exceed 30%.

Key tax rates at a glance:

- Corporate income tax: 10% flat rate, no minimum tax

- Personal income tax: 10% flat rate, no progressive scale

- Dividend withholding tax: 5% on distributed profits

- Standard VAT: 20%; reduced 9% on qualifying goods and services

- VAT registration threshold: EUR 51,130 annual turnover

- Employee social security: 13.78% of gross salary

- Employer social security: 18.92%–19.62% of gross salary

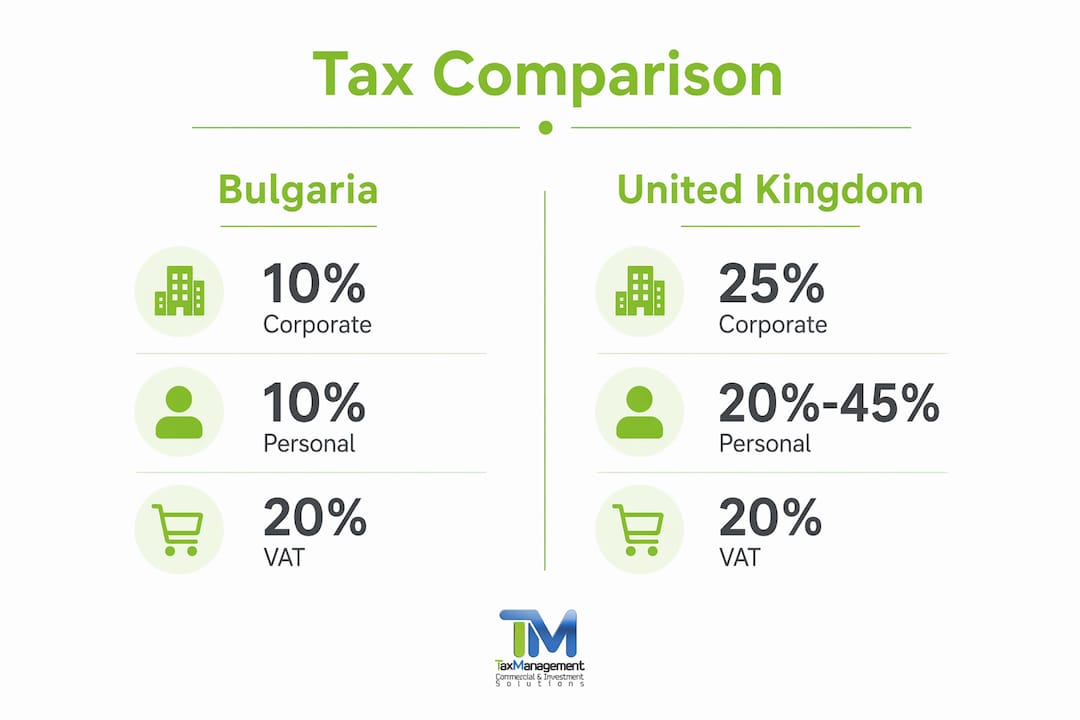

How does Bulgaria compare to the UK on corporate and personal tax?

Bulgaria and the United Kingdom represent opposite ends of the EU and post-EU tax spectrum. The comparison is instructive for any entrepreneur weighing jurisdictional options.

| Tax Category | Bulgaria | United Kingdom |

|---|---|---|

| Corporate income tax | 10% flat | 25% main rate (19% for small profits under £50,000) |

| Personal income tax | 10% flat, no threshold | 20%–45% progressive, with personal allowance |

| Dividend tax | 5% withholding | 8.75%–39.35% depending on income band |

| Standard VAT | 20% | 20% |

| VAT registration threshold | EUR 51,130 | £90,000 |

| Employer social security | 18.92%–19.62% | 13.8% (National Insurance) |

The personal income tax comparison is equally significant. A UK director drawing a salary above £125,140 faces a 45% marginal rate. The same individual, if structured as a Bulgarian resident receiving Bulgarian-sourced income, pays 10% on the full amount. The flat tax regime eliminates bracket management entirely, reducing both the compliance burden and the need for complex salary structuring.

The UK’s VAT registration threshold of £90,000 is considerably higher than Bulgaria’s EUR 51,130, meaning smaller UK businesses can trade without VAT registration for longer. However, for established businesses with turnover well above both thresholds, this difference is largely administrative rather than financial.

Pro Tip: If you are considering relocating a holding structure to Bulgaria, confirm your tax residency status with a qualified advisor before filing. Residency is determined by incorporation location and management control, not just the nationality of the shareholders.

What are the 2026 compliance requirements and key deadlines?

Meeting Bulgarian tax obligations requires adherence to specific filing and payment schedules. The rules changed in 2026, and businesses must update their internal calendars accordingly.

- Annual corporate tax return deadline. The filing deadline for the annual corporate income tax return moved from March 31 to June 30. This extension gives companies additional time to finalize financial statements and coordinate with accountants before submission.

- Advance tax payment schedule. Advance payments are calculated based on prior-year turnover. Companies with turnover below EUR 153,387 are exempt from advance payments. Companies with turnover between EUR 153,387 and EUR 1,533,876 make quarterly advance payments. Companies exceeding EUR 1,533,876 in turnover make monthly advance payments. These thresholds are based on the previous tax year’s results, so a company that crosses a threshold mid-growth must adjust its payment schedule for the following year.

- New company exemption. Newly incorporated companies are exempt from advance corporate tax payments in their first year of operation. This exemption does not apply to companies formed through a transformation or restructuring of an existing entity. For genuine startups, this rule provides meaningful cash flow relief during the initial trading period.

- Withholding tax on dividends. The 5% withholding tax on dividends must be declared and remitted by the distributing company, not the recipient. The payment deadline is the end of the month following the month in which the dividend was resolved. Late payment attracts statutory interest, so timely remittance is a compliance priority.

- Social security reporting and payment. Employer social security contributions are reported and paid monthly, alongside employee payroll withholdings. The reporting deadline is the 25th of the month following the payroll period. Employers must submit declarations to the National Revenue Agency (NRA) and the National Social Security Institute (NSSI) on a monthly basis.

- VAT filing. VAT-registered businesses file monthly VAT returns with the NRA. The deadline is the 14th of the month following the reporting period. Businesses with turnover below the registration threshold are not required to register but may choose to do so voluntarily if it benefits their input tax recovery position.

What tax incentives can businesses leverage in Bulgaria?

Bulgaria’s tax code includes several provisions that go beyond the headline flat rate and offer concrete planning opportunities for businesses operating in 2026.

- Accelerated depreciation for electric vehicles. From January 1, 2026, businesses can apply a 50% annual depreciation rate to electric vehicles. A company purchasing an electric vehicle fleet can write off half the asset value in year one, reducing taxable profit significantly. This provision aligns with Bulgaria’s green transition commitments and provides a direct tax planning tool for businesses planning vehicle upgrades.

- No minimum corporate tax. Bulgaria imposes no minimum tax and no alternative minimum calculation. A company that reports a loss in a given year pays zero corporate tax for that year. Loss carryforward provisions allow unused losses to offset future profits, providing further flexibility for businesses in early growth phases.

- Stable dividend tax rate. The 5% dividend rate held firm in 2026 despite legislative proposals to increase it. This stability allows shareholders to model profit distribution costs with confidence. The predictability of the rate is itself a planning advantage, as it removes the need to accelerate distributions ahead of anticipated rate changes.

- Flat tax simplicity as a cost reduction. The simplicity of Bulgaria’s flat-rate system reduces the administrative cost of tax compliance. Companies do not need to model marginal rates, manage bracket thresholds, or restructure compensation packages to minimize progressive tax exposure. This translates directly into lower accounting fees and reduced management time spent on tax planning.

- Euro adoption trajectory. Bulgaria is advancing toward euro adoption, which will eliminate currency conversion costs for EU-based transactions and simplify cross-border accounting for companies operating across multiple EU member states.

Pro Tip: Businesses purchasing electric vehicles in 2026 should document the acquisition and classify assets correctly under Bulgarian accounting standards to qualify for the 50% accelerated depreciation. Misclassification as a non-qualifying asset forfeits the benefit entirely.

For entrepreneurs evaluating single-member company structures in Bulgaria, the combination of flat personal and corporate tax rates creates a particularly efficient structure for owner-managed businesses.

Key Takeaways

Bulgaria’s flat 10% corporate and personal tax rates, combined with a 5% dividend tax, produce a total distributed profit burden of 14.5%, making it the most tax-efficient corporate jurisdiction in the EU.

| Point | Details |

|---|---|

| Flat 10% corporate tax | Bulgaria applies a uniform 10% rate with no minimum tax or progressive brackets. |

| Combined profit distribution burden | Corporate tax plus dividend withholding produces a 14.5% total burden on distributed profits. |

| 2026 filing deadline extended | The annual corporate tax return is now due June 30, giving businesses more preparation time. |

| Advance payment thresholds | Companies below EUR 153,387 turnover are exempt; larger companies pay quarterly or monthly. |

| 2026 EV depreciation incentive | Electric vehicles qualify for 50% annual accelerated depreciation starting January 1, 2026. |

How Taxmanagement can support your Bulgarian tax compliance

Taxmanagement has supported more than 1,500 international businesses in establishing and maintaining compliant operations in Bulgaria over more than 20 years of practice. The firm’s team of legal, accounting, and IT professionals covers the full scope of Bulgarian corporate tax compliance, from initial company registration through annual filing, advance payment scheduling, and VAT management.

For businesses evaluating the OOD company structure or planning a full relocation of their EU holding entity, Taxmanagement provides structured advisory services that address both Bulgarian regulatory requirements and cross-border EU compliance obligations. The firm’s approach reduces the administrative burden on management teams while maintaining full compliance with National Revenue Agency requirements. Contact Taxmanagement through taxmanagement.eu to discuss your specific compliance and tax planning requirements for 2026.

FAQ

What is the corporate tax rate in Bulgaria in 2026?

Bulgaria applies a flat 10% corporate income tax rate in 2026, with no minimum tax and no progressive scale. This is the lowest corporate tax rate among EU member states.

How does the Bulgarian dividend tax work?

The dividend withholding tax rate is 5%, applied to profit distributions from Bulgarian companies to shareholders. Combined with the 10% corporate tax, the total burden on distributed profits is 14.5%.

When is the Bulgarian corporate tax return due?

The annual corporate income tax return deadline is June 30, following a 2026 change that extended the previous March 31 deadline. This applies to all resident companies filing for the prior tax year.

Are new companies exempt from advance tax payments in Bulgaria?

Yes. Newly incorporated companies are exempt from advance corporate tax payments in their first year of operation, provided they were not formed through a restructuring or transformation of an existing entity.

What is the VAT registration threshold in Bulgaria?

Businesses must register for VAT once annual turnover exceeds EUR 51,130. Voluntary registration is permitted below this threshold and may benefit companies with significant input VAT to recover.