Foreign firms in Bulgaria must comply with mandatory annual financial disclosures, advance tax payments, and inactivity declarations to avoid penalties. They must also ensure foreign documents are properly notarized, translated, and submitted electronically, with deadlines closely tracked. The EU sustainability reporting rule will impact non-EU parent companies operating in Bulgaria starting in 2029.

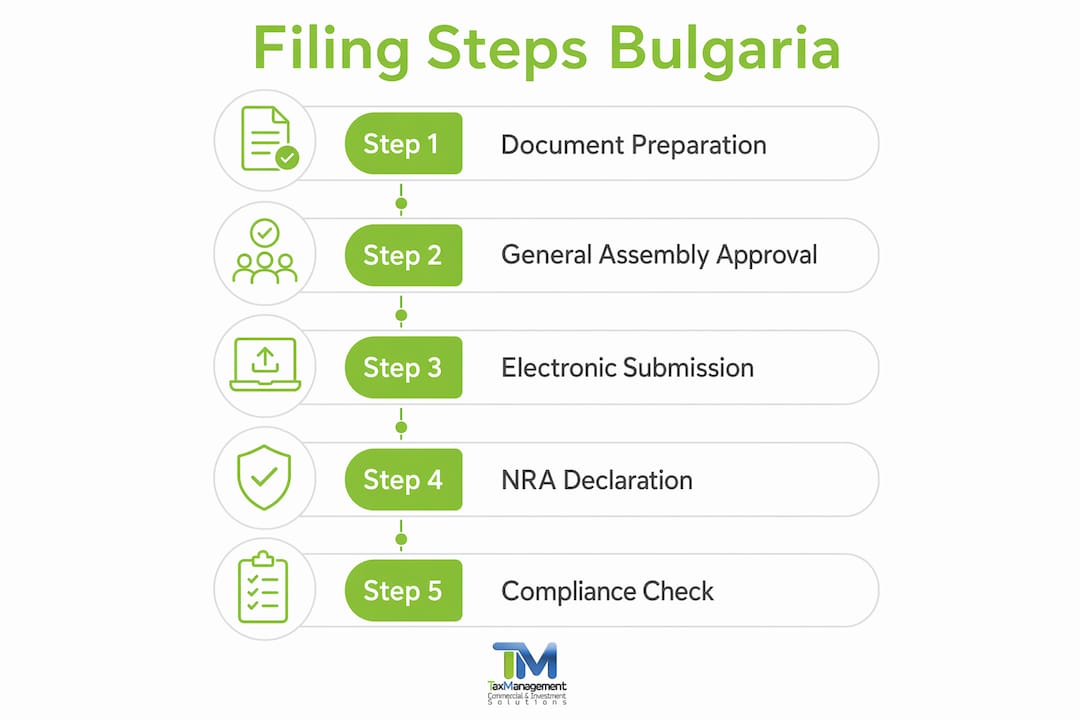

Bulgaria financial reporting obligations for foreign firms are defined as the legally mandated set of annual, quarterly, and event-driven disclosures that every company registered in the Bulgarian Commercial Register must fulfill, regardless of where its parent entity is incorporated. This includes branches of foreign traders, single-member limited liability companies (EOODs), and multi-member limited liability companies (OODs). The framework covers annual financial statement filing, advance corporate income tax payments, and declarations of inactivity for dormant entities. Non-compliance triggers fines for both the company and its management. Foreign investors who treat Bulgarian compliance as secondary to their home-country filings routinely face penalties that could have been avoided with basic planning.

What are the annual financial statement filing requirements for foreign firms in Bulgaria?

Every company registered in Bulgaria must publish annual financial statements by september 30 following the reporting year. This deadline applies even to companies with zero activity. The filing process has two distinct stages, and missing either one creates compliance exposure.

Stage one: approval. The company’s General Assembly must convene and approve the financial statements by june 30. The timing of this meeting varies slightly by company type. An EOOD, which has a single owner, can approve statements by a written decision of the sole owner. An OOD requires a formal General Assembly meeting with documented minutes.

Stage two: filing. After approval, the company files the statements with the Bulgarian Commercial Register by september 30. The filing must include:

- Audited or unaudited financial statements (depending on company size thresholds)

- A declaration confirming the statements were approved

- Amended articles of association, if the company has not yet completed the mandatory capital redenomination from Bulgarian Lev to Euro required in 2026

- Supporting resolutions from the General Assembly or sole owner

The 2026 capital redenomination requirement deserves specific attention. Bulgarian law now requires all companies to file amended articles of association reflecting the conversion of share capital from BGN to EUR alongside their first 2026 Commercial Register application. Failure to include this document causes the entire filing to be rejected. This is not a one-time administrative formality. It directly affects whether your annual financial statement submission is accepted at all.

Foreign directors face an additional procedural layer. Foreign-originated documents submitted to the Commercial Register must be notarized, apostilled, and translated into Bulgarian by a certified sworn translator. Electronic signatures alone do not satisfy this requirement. A foreign director does not need to travel to Bulgaria to complete this process. A local representative holding a notarized power of attorney can handle the submission on their behalf.

All declarations filed with the National Revenue Agency (NRA) must be submitted electronically using a qualified electronic signature, known in Bulgarian as a КЕП. Paper filings are no longer accepted by the NRA. Foreign managers can obtain a cloud-based КЕП remotely, which makes full remote compliance achievable without traveling to Bulgaria.

Pro Tip: Coordinate the capital redenomination filing with your annual financial statement submission. Filing them together in one Commercial Register application saves time and avoids a second round of notarization and apostille costs.

Late filing carries financial consequences for both the entity and its management. Fines for companies range from €100 to €2,550. Fines for managers range from €100 to €500. These fines begin accumulating immediately after the deadline passes.

| Obligation | Deadline | Responsible Party |

|---|---|---|

| General Assembly approval of statements | june 30 | Company owners or shareholders |

| Filing with Commercial Register | september 30 | Company management |

| Capital redenomination (amended articles) | With first 2026 filing | Company management |

| Electronic filing via КЕП | Ongoing | Authorized signatory |

How do advance corporate income tax payments affect foreign companies in Bulgaria?

Bulgaria operates a pay-as-you-go corporate income tax system. Foreign companies registered in Bulgaria are subject to the same advance payment rules as domestic firms. The obligation to make advance payments depends on the company’s annual turnover from the prior year.

The thresholds work as follows:

- No advance payments required: Companies with turnover below €153,387 in the prior year are exempt from advance payments.

- Quarterly advance payments: Companies with turnover between €153,387 and €1,533,876 must pay quarterly installments.

- Monthly advance payments: Companies with turnover above €1,533,876 must pay monthly installments.

Quarterly payments are due by the 15th of the month following each quarter. Monthly payments are due by the 15th of each month. The annual corporate income tax return and any remaining balance are due by june 30 of the following year.

Newly established companies are exempt from advance payments in their first year of operation and in the year following establishment. This exemption gives new foreign-owned entities time to establish cash flow before the advance payment cycle begins.

The penalty for underpayment is calculated on the shortfall amount from april 16 to december 31 of the tax year. Penalty interest applies when the advance payments made are more than 25% below the final tax liability. The interest rate equals the Bulgarian National Bank base rate plus 10 percentage points. This is not a trivial amount if a company significantly underestimates its taxable income.

Pro Tip: If your company’s profitability is expected to drop significantly compared to the prior year, Bulgarian tax law allows you to apply for a reduction in advance payment amounts. Filing this request early with the NRA avoids overpaying and then waiting for a refund.

Accurate income forecasting is the most practical way to avoid penalty interest. Companies that track monthly revenue against prior-year figures can adjust their advance payments before the 25% threshold is breached. This requires coordination between the company’s accounting function and its management, which is often a gap for foreign-owned entities operating with remote oversight.

What are the reporting obligations for dormant or inactive foreign companies in Bulgaria?

Dormancy does not suspend a company’s compliance obligations in Bulgaria. This is the single most common misconception among foreign investors who register a Bulgarian entity and then pause operations. A company that has had no transactions, no revenue, and no employees in a given year still has active filing obligations.

The primary obligation for an inactive company is the Declaration of Inactivity. This declaration must be filed with both the Commercial Register and the NRA by june 30 following the inactive year. Filing this declaration exempts the company from submitting a full set of annual financial statements. That exemption is significant because it reduces both the cost and the administrative burden of compliance for a year with no activity.

Key points for foreign investors managing dormant Bulgarian entities:

- The declaration must be filed even if the company had zero revenue and zero transactions for the entire year.

- Missing the june 30 deadline exposes the company and its management to the same fines as active companies: €100 to €2,550 for the entity and €100 to €500 for management.

- The declaration does not replace the obligation to file a corporate income tax return if any taxable income existed during the year.

- Companies that fail to file the declaration are treated as active by default and must submit full financial statements retroactively.

Foreign investors who hold Bulgarian entities as part of a broader EU structure sometimes assume that inactivity at the Bulgarian level is self-evident to authorities. It is not. The NRA and the Commercial Register have no mechanism to distinguish between a company that forgot to file and one that genuinely had no activity. Both are treated identically until the declaration is submitted.

Pro Tip: Set a calendar reminder for may 15 each year to assess whether your Bulgarian entity was inactive in the prior year. That gives you six weeks to prepare and file the Declaration of Inactivity before the june 30 deadline.

How does the EU Corporate Sustainability Reporting Directive affect foreign firms in Bulgaria?

The EU Corporate Sustainability Reporting Directive (CSRD) extends sustainability reporting obligations to non-EU parent companies with significant activities within the European Union. For foreign firms operating in Bulgaria, this represents a new layer of compliance that sits above the existing Bulgarian financial reporting framework.

The CSRD timeline for non-EU companies begins in 2029, covering financial years from 2028 onward. An estimated 1,200 non-EU companies will fall within scope. The trigger is having substantial EU-based revenue or a significant EU subsidiary. A foreign firm with a Bulgarian operating company that generates meaningful revenue may qualify.

Practical implications for foreign investors with Bulgarian operations include:

- Sustainability data collection must begin well before the 2029 reporting deadline to build a credible baseline.

- The CSRD requires reporting under the European Sustainability Reporting Standards (ESRS), which cover environmental, social, and governance metrics.

- Bulgarian subsidiaries of non-EU parents will need to provide data to the parent for consolidation into the group-level sustainability report.

- Companies structured as OODs or EOODs in Bulgaria should assess whether their EU revenue thresholds bring them into CSRD scope.

The CSRD does not replace Bulgarian financial reporting requirements. It adds a parallel obligation at the EU level. Foreign firms planning long-term operations in Bulgaria should factor CSRD readiness into their compliance planning now, rather than treating it as a 2028 problem.

Key Takeaways

Foreign firms in Bulgaria face a layered compliance framework that requires active management of annual filings, advance tax payments, and inactivity declarations, with penalties applying regardless of business activity level.

| Point | Details |

|---|---|

| Annual filing deadline | Approve financial statements by june 30 and file with the Commercial Register by september 30. |

| Advance tax thresholds | Quarterly payments apply above €153,387 turnover; monthly payments apply above €1,533,876. |

| Dormant company obligations | File a Declaration of Inactivity by june 30 to avoid full financial statement requirements and penalties. |

| Document legalization | Foreign-originated documents require notarization, apostille, and certified Bulgarian translation before submission. |

| CSRD preparation | Non-EU parent companies with significant EU activity face sustainability reporting obligations starting in 2029 for FY 2028. |

How Taxmanagement can help you meet Bulgaria’s compliance deadlines

Bulgaria’s compliance calendar is specific, deadline-driven, and unforgiving for foreign firms managing operations remotely. Taxmanagement has supported more than 1,500 international businesses with company registration and accounting services in Bulgaria, drawing on over 20 years of experience with both Bulgarian and EU regulatory requirements. The team handles annual financial statement preparation and filing, advance tax payment calculations, Declaration of Inactivity submissions, and the 2026 capital redenomination process. For foreign directors who need remote compliance support, Taxmanagement facilitates cloud-based КЕП setup and document legalization coordination. If you are managing a Bulgarian entity from abroad and want to avoid the penalties that come with missed deadlines, contact Taxmanagement directly at taxmanagement.eu to discuss your specific situation. You can also explore the benefits of outsourced accounting to understand how professional support reduces compliance risk.

FAQ

What is the annual financial statement filing deadline in Bulgaria?

Companies must have their financial statements approved by june 30 and filed with the Bulgarian Commercial Register by september 30 of the year following the reporting period. Both deadlines apply to all registered entities, including branches of foreign traders.

Do dormant foreign companies in Bulgaria need to file anything?

Yes. A dormant company must file a Declaration of Inactivity with both the Commercial Register and the NRA by june 30. Missing this deadline results in the same fines as those applied to active companies.

What triggers advance corporate income tax payments in Bulgaria?

Companies with prior-year turnover above €153,387 must make quarterly advance payments. Companies with turnover above €1,533,876 must make monthly payments. The final annual tax return is due by june 30.

Can foreign directors manage Bulgarian compliance remotely?

Yes. Foreign directors can obtain a cloud-based qualified electronic signature (КЕП) remotely and authorize a local representative via notarized power of attorney to handle Commercial Register submissions without traveling to Bulgaria.

When does the EU CSRD apply to non-EU companies with Bulgarian operations?

The CSRD applies to non-EU ultimate parent companies with significant EU activities starting in 2029 for financial years from 2028 onward. An estimated 1,200 non-EU companies fall within the initial scope of this requirement.