Summary

- An LLC is a business structure that combines liability protection with pass-through taxation. It shields personal assets from business debts and lawsuits, with profits passing directly to members for tax reporting. Proper formation and an operating agreement are essential to maintain its legal protections and operational continuity.

A limited liability company, commonly known as an LLC, is defined as a distinct business structure created under state law that combines the personal liability protection of a corporation with the pass-through taxation of a partnership. Understanding the full limited liability company meaning is one of the most practical steps any entrepreneur can take before registering a business. The SBA describes an LLC as a structure that lets owners combine the benefits of both corporate and partnership models. This guide covers the LLC definition, its tax treatment, how it compares to other structures, and what entrepreneurs need to know before forming one.

What is limited liability company meaning in legal terms?

A limited liability company is a hybrid business entity that provides its owners, called members, with a legal shield against personal liability for business debts and lawsuits. The word “limited” in the name refers directly to this protection. It limits how far a creditor or claimant can reach into a member’s personal finances.

In a sole proprietorship or general partnership, the owner carries unlimited personal liability. That means a creditor can pursue the owner’s home, vehicle, savings account, or other personal assets to satisfy a business debt. An LLC eliminates that exposure in most circumstances. The SBA contrasts this directly, noting that sole proprietorships carry unlimited personal liability while LLCs do not.

The LLC is also legally distinct from both corporations and partnerships. It is not simply a renamed version of either. Each state has its own LLC statute, which governs how the entity is formed, managed, and dissolved. Legal forms of companies in Bulgaria follow a parallel logic, with the Bulgarian OOD (Дружество с ограничена отговорност) serving as the closest equivalent to the American LLC.

How does limited liability actually protect your personal assets?

Limited liability protection means that if your business is sued or cannot pay its debts, your personal assets are generally off limits. The business’s creditors can only pursue what the business owns, not what you own personally.

Assets typically protected under an LLC structure include:

- Your primary residence and any real estate held personally

- Personal vehicles not titled to the business

- Personal bank accounts and savings

- Personal investment portfolios and retirement accounts

This protection is not absolute. Courts can “pierce the corporate veil,” a legal doctrine that removes the liability shield when owners blur the line between personal and business finances. Failure to observe legal formalities, such as commingling funds or failing to maintain proper records, can expose owners to personal liability even within an LLC.

Pro Tip: Open a dedicated business bank account the day you form your LLC. Mixing personal and business funds is the single most common reason courts pierce the corporate veil and hold members personally liable.

How is an LLC taxed, and what does pass-through taxation mean?

Pass-through taxation is the defining tax feature of an LLC. The business itself does not pay federal income tax. Instead, profits and losses pass directly to the members, who report them on their personal tax returns.

The IRS applies different default rules depending on the number of members:

- A single-member LLC is treated as a disregarded entity. The IRS taxes it like a sole proprietorship, using Schedule C.

- A multi-member LLC is taxed as a partnership by default, with each member receiving a Schedule K-1 showing their share of income or loss.

This structure avoids the double taxation that C corporations face, where the corporation pays tax on profits and shareholders pay tax again on dividends. Bank of America notes that this flow-through taxation is one of the primary advantages of the LLC structure.

Members of an LLC who are actively involved in the business typically owe self-employment tax on their share of profits. This covers Social Security and Medicare contributions. The IRS tax classification for an LLC can also be changed by election. Members may choose to have the LLC taxed as an S corporation or C corporation, which can reduce self-employment tax in certain situations. Understanding micro enterprise taxation rules is equally relevant for entrepreneurs registering in EU jurisdictions like Bulgaria.

Pro Tip: Consult a tax professional before electing corporate tax treatment for your LLC. The self-employment tax savings can be real, but the added compliance costs and payroll requirements may outweigh the benefit for smaller businesses.

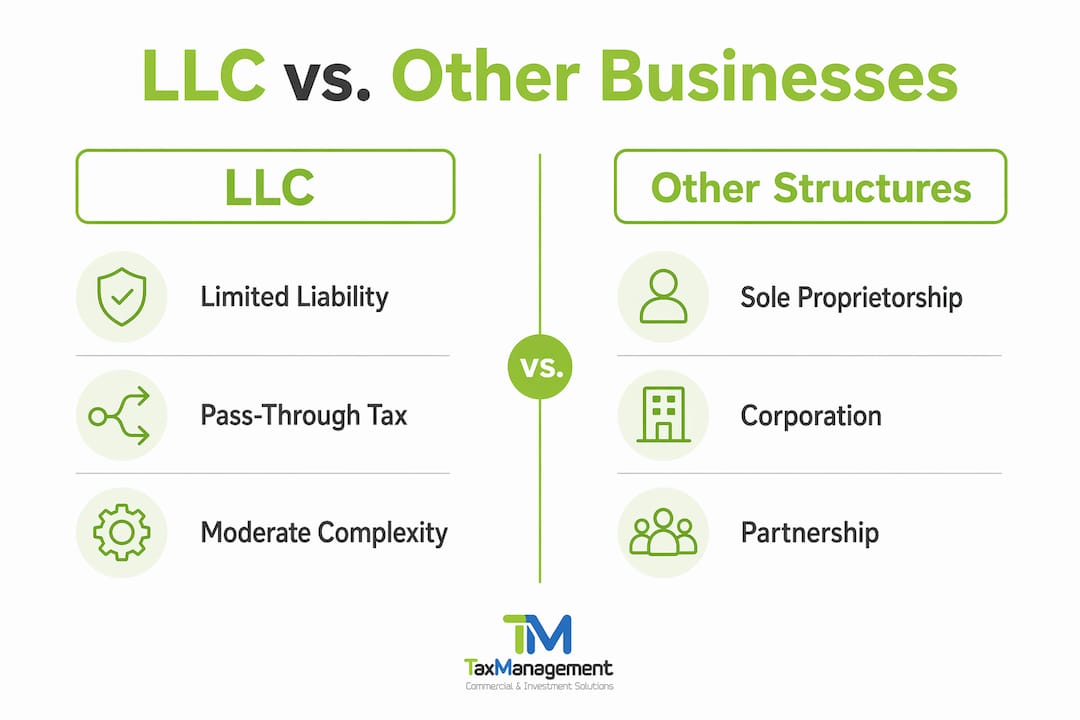

How does an LLC compare to other business structures?

The LLC sits between a sole proprietorship and a corporation on the spectrum of complexity and protection. Each structure has distinct trade-offs in liability, taxation, and administrative burden.

| Business structure | Personal liability | Tax treatment | Formation complexity |

|---|---|---|---|

| Sole proprietorship | Unlimited | Pass-through (Schedule C) | Minimal |

| General partnership | Unlimited | Pass-through (Schedule K-1) | Low |

| LLC | Limited | Pass-through (default) or corporate election | Moderate |

| S corporation | Limited | Pass-through | Higher |

| C corporation | Limited | Double taxation | Highest |

The LLC offers a middle path. It provides liability protection comparable to a corporation, with far fewer formalities. Investopedia identifies the LLC’s combination of liability shield and pass-through taxation as the core reason it has become the most popular business structure for small and medium-sized businesses in the United States.

Understanding why company structure matters for tax liability is especially relevant for international entrepreneurs who may be choosing between structures across multiple jurisdictions.

Pro Tip: If you plan to raise venture capital or issue stock options to employees, a C corporation is typically the better choice. Investors and equity compensation programs are structured around corporate shares, not LLC membership interests.

What are key practical considerations for forming and operating an LLC?

Forming an LLC requires filing articles of organization with the appropriate state agency and paying a filing fee. The process is straightforward, but the ongoing compliance obligations deserve equal attention.

The five most important practical steps for LLC formation and operation are:

- File articles of organization with your state’s secretary of state office and pay the required fee, which varies by state.

- Draft an operating agreement that governs how the LLC is managed, how profits are distributed, and what happens when a member leaves or dies.

- Obtain an Employer Identification Number (EIN) from the IRS, even if you have no employees, since most banks require it to open a business account.

- Maintain separate financial records by keeping all business income and expenses in a dedicated business account.

- File annual reports and pay any required state fees to keep the LLC in good standing.

The operating agreement deserves special attention. Without one, your LLC is governed entirely by your state’s default LLC statutes. Those defaults may not reflect your intentions. The SBA warns that some states dissolve an LLC automatically if a member leaves or dies, unless the operating agreement contains specific continuity provisions. Without those terms, member changes can trigger dissolution and require re-formation, creating significant administrative disruption.

Pro Tip: Have a licensed attorney draft or review your operating agreement before you sign it. A generic template found online may miss state-specific requirements or fail to address critical scenarios like member buyouts or business succession.

What are the main benefits of forming an LLC?

The LLC structure is attractive for medium and higher-risk businesses and for any entrepreneur with significant personal assets to protect. Its core advantages are well established and consistently cited by legal and financial professionals.

Key benefits of forming an LLC include:

- Personal asset protection. Members are not personally responsible for business debts or legal judgments in most circumstances.

- Pass-through taxation. Profits flow directly to members without a corporate-level tax, avoiding double taxation.

- Flexible management. An LLC can be managed by its members or by appointed managers, giving owners control over governance structure.

- Fewer formalities. Unlike corporations, LLCs do not require annual shareholder meetings, formal minutes, or a board of directors.

- Credibility. Operating as an LLC signals a level of professionalism and commitment that a sole proprietorship does not convey.

The LLC’s main value lies in combining liability protection with pass-through taxation, though members must account for self-employment taxes on active income. For entrepreneurs with personal real estate, savings, or other assets at risk, the liability shield alone justifies the formation cost and compliance effort.

Pro Tip: Review your LLC’s operating agreement and state filings every two to three years. Business circumstances change, and an outdated agreement can create gaps in your liability protection or trigger unintended tax consequences.

Key Takeaways

An LLC is the most practical business structure for entrepreneurs who need personal asset protection without the complexity and double taxation of a corporation.

| Point | Details |

|---|---|

| LLC definition | An LLC is a state-created entity combining limited personal liability with pass-through taxation. |

| Liability protection | Members’ personal assets are shielded from business debts and lawsuits in most circumstances. |

| Tax treatment | Profits pass directly to members by default, avoiding corporate-level income tax. |

| Operating agreement | A well-drafted operating agreement is required to protect the liability shield and ensure business continuity. |

| Formation requirement | Filing articles of organization and maintaining separate finances are the two most critical formation steps. |

How Taxmanagement supports LLC-equivalent formation in Bulgaria

Entrepreneurs who want the liability protection and tax efficiency of an LLC structure within the EU have a direct equivalent in Bulgaria’s OOD (limited liability company). Taxmanagement has assisted more than 1,500 firms with company registration and compliance in Bulgaria over more than 20 years. The team combines legal, accounting, and IT expertise to handle formation, ongoing compliance, and tax optimization for businesses operating within EU regulations. For entrepreneurs who need professional support with formation documents, accounting, or fiscal planning, Taxmanagement’s consulting services with professional indemnity provide structured guidance at every stage. Contact the team directly through the accounting services page to discuss your specific requirements.

FAQ

What does LLC stand for?

LLC stands for limited liability company. It is a business structure created under state law that protects its owners from personal liability for business debts and obligations.

Is an LLC the same as a corporation?

An LLC is not a corporation. It shares the liability protection of a corporation but avoids double taxation and requires fewer formal compliance obligations.

Can a single person form an LLC?

Yes. A single-member LLC is a recognized structure under IRS rules and is taxed as a disregarded entity by default, meaning the owner reports business income on a personal tax return.

What happens to an LLC when a member leaves?

Some states dissolve an LLC automatically when a member exits unless the operating agreement contains specific continuity provisions. A well-drafted agreement prevents this outcome.

Do LLC members pay self-employment tax?

Yes, in most cases. Members who actively participate in the business owe self-employment tax on their share of profits, covering Social Security and Medicare contributions.